- What is liquidity?

- How does liquidity work?

- Why do Brokers need liquidity?

- How to choose and compare Liquidity Providers?

- What are the types/classes of financial instruments? What are the differences between them? Which ones are the most popular?

- Tier 1, Prime Brokers, Prime of Prime Brokers

- Notional Volume, Lot, Base Currency, Yard and other definitions

- How to calculate a fee per million?

- What spreads/markups/commissions should be set by the Broker for A-Book and B-Book models?

- A-Book / B-Book / C-Book (revenue share model)? What are the pros and cons of each of them? In which situations should you consider these models?

- How to calculate how much a broker will earn when hedging?

- How to spot good and bad timing for B-Book? How to control the risk and exposure?

What is liquidity? #

Liquidity in financial markets can be understood as the number of orders placed by various market participants in a Financial Instrument. Higher liquidity is desirable for everyone on the market. It drives down the spreads and the cost of trading. EURUSD and GOLD are considered to have the highest liquidity as there are many market participants and orders placed by them both on the Buy and Sell sides. A liquidity provider is, by definition, a market broker or institution which behaves as a market maker in a chosen asset class. Practically speaking, liquidity providers grant liquidity to retail brokers, enabling them to hedge their client trades and mitigate their market risk.

How does liquidity work? #

Liquidity is the number of buyers and sellers within a market. For example, if there are more buyers and sellers in Asset 1 compared to Asset 2, we can say that Asset 1 has more liquidity than Asset 2. Liquidity is built in the orderbook using limit orders, so a liquidity provider giving liquidity to a broker allows executing trades at prices and volumes visible in the orderbook. Brokers who hit the orderbook are liquidity takers because each completed order decreases the liquidity.

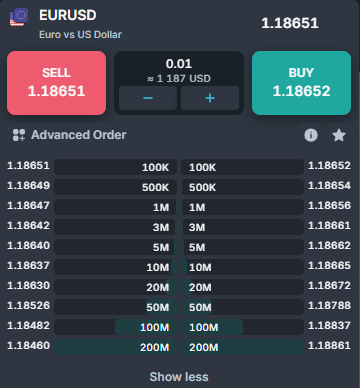

In the image above, Broker can see a sample orderbook of the EURUSD instrument. He can use it to check what volume can be executed at exactly what price. If an order is bigger than 500k (5 lots), then the client will consume more than one orderbook line, and he will receive a VWAP (Volume Weighted Average Price).

Buy orders sent by clients always hit the right side of the orderbook (Ask Prices). Sell orders always hit the left side of the orderbook (Bid Prices). In other words, BIDs are the buy offers, and ASKs are the sell offers, both placed in the orderbook. Each order placed in the orderbook always has its price and volume. It provides information on how much traders can execute at a given price.

The difference between the bid and ask prices is called a spread. In the image above, the spread is 42 points (1.06030 – 1.05988). It is worth mentioning that for bigger orders, which exceed the volume available at the first line, the spread will be higher as it is calculated based on the VWAP.

How to calculate the Volume Weighted Average Price? Example

Market Order Buy 800k EURUSD will be executed according to the Orderbook.

500k executed @ 1.06010

300k executed @ 1.06011

VWAP = (500 x 1.06010 + 300 x 1.0611) / 800 = 1.060104

Why do Brokers need liquidity? #

Retail Brokers usually need liquidity to hedge their market exposure or profitable/toxic clients in order to optimise their company’s P/L and minimise the risk.

When a Broker signs a liquidity agreement, it receives both pricing and trading sessions. It is also allowed to use the pricing session to provide execution for his B-Book trades.

If a Broker wants to start hedging, it needs to have an adequate margin on its liquidity (hedge) account, which is opened with the liquidity provider. If the margin on the hedge account is insufficient, trades can be rejected, or, in extreme cases, Broker can face a Margin Call or even Stop Out on its account.

To top up the hedge account, Broker needs to have its own capital or transfer some of the funds deposited by its clients.

Why is it important to have liquidity, especially for startup brokers?

Let’s face it! The Forex Retail Broker industry is fiercely competitive, and startups often lack expertise in IT and dealing. If such a broker accepts high-risk clients, its profitability can be jeopardised. In some cases, this may even lead to default if the Broker doesn’t have sufficient internal capital.

Just a few big clients generating a profit is enough to create a problem for your company. That’s why startup Brokers usually do full STP (only A-Book) until they get a diversified portfolio of clients. After gaining the appropriate experience and acquiring additional funds, you can proceed to diversify the risk.

How to choose and compare Liquidity Providers? #

With an increasing number of retail brokers, the number of liquidity providers is also rapidly growing. Many available options make it possible to choose a supplier perfectly suited to your needs. How to choose the perfect liquidity provider? Retail Brokers usually compare LPs by checking the following variables:

- Financial instruments offering (what scope of markets is offered)

- Trading conditions (leverage, NOP limits, min/max size of transactions)

- Commission per million

- Spreads (maximum spread, news)

- Swaps (charged per day, no triple swaps on Wednesdays)

- Overall Cost

- Execution Quality (slippage symmetry)

- Speed of Execution

- Server Down Times – reliability

- Good Financial Standing (balance sheet)

- Reputation

- Additional Services (swap free, credit facility, technology solutions etc.)

What are the types/classes of financial instruments? What are the differences between them? Which ones are the most popular? #

All of the trading instruments available for retail brokers are CFDs. A Contract For Difference (CFD) is a contract between a buyer and a seller instructing that the buyer must pay the seller the difference between the current value of an asset and its value at contract time. CFDs allow traders and investors to profit from price movement without owning the underlying assets.

We distinguish a few asset classes in the CFD instruments:

- Forex Spot Instruments (e.g. EURUSD, GBPUSD etc.)

- Metal Spot Instruments (e.g. GOLD, SILVER etc.)

- Futures on Commodities and Global Indices (FUT NASDAQ 100. FUT CORN)

- Cash Commodities and Global Indices (these are instruments based on the Index price or Spot price, not a Future price, e.g. CASH DOWJONES30)

- Shares (CFDs on popular Shares listed on various exchanges, e.g. BMW, Apple etc.)

- Cryptos (CFDs on popular cryptocurrencies, such as BTC, ETH, etc.)

The most significant dividing lines between Futures and Cash/Spot instruments:

- Future Value vs Current Value – The difference lies in the method of calculating the price.

- Expirations/rollovers – Future contracts always have an expiration date until which the instrument is valid. If a client has a position and the expiration date is approaching, the Broker must either roll it over to the next contract or settle the position at the expiration price.

Top instruments. Why are they so popular?

- EURUSD, GBPUSD – High Liquidity/Volatility.

- XAUUSD – High Liquidity/Volatility.

- NASDAQ, DJ30, S&P500, DAX – High Liquidity/Volatility, very popular benchmarks which track broader markets’ performance.

- Shares – They represent popular companies that are well-known in the market.

- Cryptos – BTC, ETH, XRP – Popular, especially among numerous younger clients.

Tier 1, Prime Brokers, Prime of Prime Brokers #

Tier 1 banks, also known as “major banks” or “global systemically important banks” (GSIBs), are the largest and most financially significant banks in the world.

Examples of Tier 1 Banks include such brands as Goldman Sachs, JP Morgan, Chase, Citigroup Deutsche Bank and a few other major global Banks.

A Prime Broker is a financial institution, usually a bank (but not necessarily), that provides settlement and clearing services for transactions executed on the Forex Interbank Market. Prime Brokers usually serve hedge funds and big institutional brokerages. They operate mainly in the FX Market.

A Prime of Prime (PoP) Broker, on the other hand, is a type of Broker that provides liquidity to smaller brokers, retail forex brokers, and other financial institutions. Prime of Prime Companies are not connected directly to the FX Interbank Market but use several liquidity connections to access it. Additionally, they provide a much wider scope of markets as they can be connected to various markets through their partnerships.

The significant advantage of having an agreement with a PoP broker is the possibility to hedge various asset classes and keep the margin only with one counterparty, aggregating all needed markets in one place.

Notional Volume, Lot, Base Currency, Yard and other definitions #

- When the commission is set to 10 USD per million USD traded, it means the volume in Notional terms.

- Base Currency is the currency which is in the first place in a given pair. For example, in the EURUSD pair, EUR is the base currency which is used to calculate notional value. In the GBPUSD pair, GBP will be a base currency.

- In institutional trading, the usual base currency is USD.

- A Yard in finance is a common phrase/measure to express the Notional Volume in Billions.

- Lot is used to calculate the “real” volume of a given transaction and per million commission (1 lot of EURUSD vs 1 lot of XAUUSD)

- Retail brokers use the lot as an easy way to understand and measure exposure for retail clients. One lot in forex instruments is usually 100,000 units of a base currency.

- How do we calculate this: Lots * Price * Contract Size in a given currency. For Example, if a Client has a trade of AUS200 with 5 lots BUY (or SELL), the contract size set to 0,25, and the price at 7237 USD, the formula to calculate will look like below: 5 x 0.25 x 7237 = 9,046.25 USD

How to calculate a fee per million? #

- The fee per million is charged per side (separately for opening order and closing order)

- How to calculate the notional USD of a client

- Contract size * Volume * Price * Conversion rate to USD

Example 1: The Client with 8$ per million opens a trade BUY 10 lots of XAUUSD at a price of 1800

- How much will the client be charged?

- 100 USD * 10 * 1800 = 1 800 000 Notional Volume in USD

- 8/1,000,000 * Notional Volume = $14.4 per side

- $28.8 round-turn (open and close)

Example 2: client with 8$ per million opens a trade BUY 5 lots of EURUSD at a price of 1.07341

- How much will the client be charged?

- 100,000 * 5 * 1.07341 (EURUSD rate) = 536 705 Notional Volume in USD

- 8/1,000,000 * Notional Volume = $4.29 per side

- $8.58 round-turn (open and close)

Example 3: client with 8$ per million opens a trade BUY 200 lots of GER30 at a price of 15200

- How much will the client be charged?

- 0.25 EUR * 200 * 15 200 * 1.07731 (EURUSD rate) = 818 755 Notional Volume in USD

- 8/1,000,000 * Notional Volume = $6.55* per side

- $13.1 round-turn (open and close)

What spreads/markups/commissions should be set by the Broker for A-Book and B-Book models? #

- Brokers using the A-Book model have to make sure that they charge more than what they get charged by the Liquidity Provider (spread Markups, swaps and commissions). In other words, the Broker needs to calculate if markups added to his clients’ accounts will be sufficient to cover the cost charged on the liquidity account. Of course, it should make some profit from them additionally, to cover his other business costs.

- Brokers using the B-Book model have to set the spreads at adequate levels to optimise the overall profitability. In the longer run, the higher the spreads/commissions, the bigger Broker’s profit should be. Of course, too high spreads & commissions can also discourage clients from trading, so it is important to optimise them in order to have them in line with the industry competition.

A-Book / B-Book / C-Book (revenue share model)? What are the pros and cons of each of them? In which situations should you consider these models? #

Full A-Book

Pros:

- Broker doesn’t have to worry about risk management. It can set the commission and markups once and then focus solely on increasing the number of clients and trading volume.

- Broker is not dependent on market conditions. It will be profitable regardless of whether the market is currently volatile or is consolidating.

- A Broker can quickly start with his own limited capital, as he sends 100% flow to the liquidity provider.

- Clear information about not having a conflict of interest increases the Brokers reputation in the eyes of traders.

Cons:

- Broker profit is dependent on the client’s volume. Favourable if your clients are day trading, but it can be an issue if they are long-term investors (it can be handled by swap markups, though).

- Broker clients have to have the same leverage that it has on the hedge account, or it will have to monitor its hedge account margin level in order not to get stop-out on the hedge account before clients would (it can be handled by increasing stop-out level to higher value vs broker hedge account).

- Brokers need to transfer money to a hedge account and request withdrawals from LP if needed.

For whom?

- For a Broker that has a lot of day traders or he is providing cashback as one of the marketing tools.

- If a broker has small starting capital, he protects himself from risk and puts all the effort into sales.

- Brokers with clients that have a concentrated trading flow.

Full B-Book

Pros:

- In the long run, the Broker’s potential profits should be approximately equal to the value of spreads and commissions charged to the clients’ accounts. Such a scenario is possible only if a broker’s portfolio is well diversified.

- Execution is not dependent on the liquidity provider (you can easily reopen clients’ trades if necessary).

Cons:

- Unlimited loss. All clients’ profits must be covered by brokers’ own capital.

- A Broker needs to monitor the risk constantly.

- A clear conflict of interest between you and your clients can make them suspicious of any malicious behaviour from your side. Suspicions of a conflict of interest can diminish your reputation.

- It is harder to acquire a licence for FX brokers using this model of execution.

- Big capital is needed to handle the risk effectively, as each Broker needs to have a capital cushion to absorb the losses from clients’ accounts.

For whom?

- Big starting capital is a must.

- A Broker needs a lot of his own exotic symbols, and LPs are not able to provide them.

C-Book (Hybrid model)

Pros:

- Combines benefits from both models by limiting the risk using a hedge account but still giving room for potentially more significant earnings from taking some of the risks on the broker side.

- You can use this hybrid model in various ways: using coverage (for example, hedging half of your client’s trades) or hedging only the customers with profitable history. You can also hedge only some symbols that you are concerned about or only the clients with high deposits or traded volumes.

- If you can correctly identify periods of no volatility and also manage the risk, you are able to adjust to current market conditions to optimise profitability.

Cons:

- You still have to put effort and time into managing the risk while taking the risk of losses.

- Unlike an A-Book broker, you can not claim that you don’t have a conflict of interest with your clients.

For whom?

- Experienced brokers with the resources to manage their risk and know their clients’ trading activity well.

- Brokers with clients that have diversified trading flow.

How to calculate how much a broker will earn when hedging? #

Commission

A broker can use various types of commissions to charge his clients (depending on units or the nominal value of a trade or pips). However, in the end, it all comes down to the quantity of clients’ volume traded.

Commission example:

X USD per 1 million USD traded is the same way of calculating as per mill but differently described.

For example, 1000 USD per 1 million trade = 1 per mil.

Let’s calculate 20 USD per 1 million traded for 3 lots of AUDNZD:

(20/1000000)x(3x100000AUD)=6AUD, which is approx. 4.06 USD

USDc per lot is 0.01 per 1 unit traded. It is good to use it for FX or for symbols that have similar nominal values for 1 lot. Let’s calculate 20 USDc per 3 lots of AUDNZD:

20 x 0.01 USD x 3 = 0.60 USD.

When we use commission counted by pips, we need to calculate pip value using instrument specification. Let’s calculate 20 pips per 3 lots of AUDNZD:

20 x 0.00001NZD x 300 000 = 60 NZD, which is approx. 37.41 USD

Markups

It’s easy to calculate how much we earn from markups by using our instrument specification. We multiply the quote precision of a symbol by a contract size and then traded volume. What is also important is the quoted currency. If it’s not the USD, it has to be converted.

After we combine earnings from commission and markups, we need to subtract the commission from the hedge account. The earnings can be checked in Pentaho reports, and it’s a good habit to encourage brokers to check the A-Book simulation there.

Markups Example:

X X USD per 1 million USD traded is the same way of calculating as per mill but differently described. For example, 1000 USD per 1 million trade = 1 per mill. Let’s calculate 20 USD per 1 million traded for 3 lots of AUDNZD:

(20/1000000)x(3x100000AUD)=6AUD, which is approx. 4.06 USD

USDc per lot is 0.01 per 1 unit traded is good to use for FX or for symbols that have similar nominal value for 1 lot. Let’s calculate 20 USDc per 3 lots of AUDNZD:

20 x 0.01 USD x 3 = 0.60 USD

When we use commission counted by pips, we need to calculate pip value using instrument specification. Let’s calculate 20 pips per 3 lots of AUDNZD:

20 x 0.00001NZD x 300 000 = 60 NZD, which is approx. 37.41 USD

It is easy to check the profitability of A-Book in the Pentaho reports.

How to spot good and bad timing for B-Book? How to control the risk and exposure? #

Black Swan events

- Rare and unpredictable events that have a major impact on the economy.

- They are often considered highly improbable or impossible based on past experiences or data.

- Black Swan events can have severe consequences, including economic downturns, political upheavals, or technological disruptions.

- Black Swan events can have a disproportionate impact due to their unexpectedness and the lack of preparation for their occurrence.

- They can result in significant changes to the status quo, including changes to societal norms, business practices, and political structures.

This is an event that comes as a big surprise, which was not predicted by almost anyone. They usually have big impacts on brokers’ profits, either positive or negative. It is always good to control the market exposure (e.g. by hedging it) to minimise the consequences if such an event occurs.

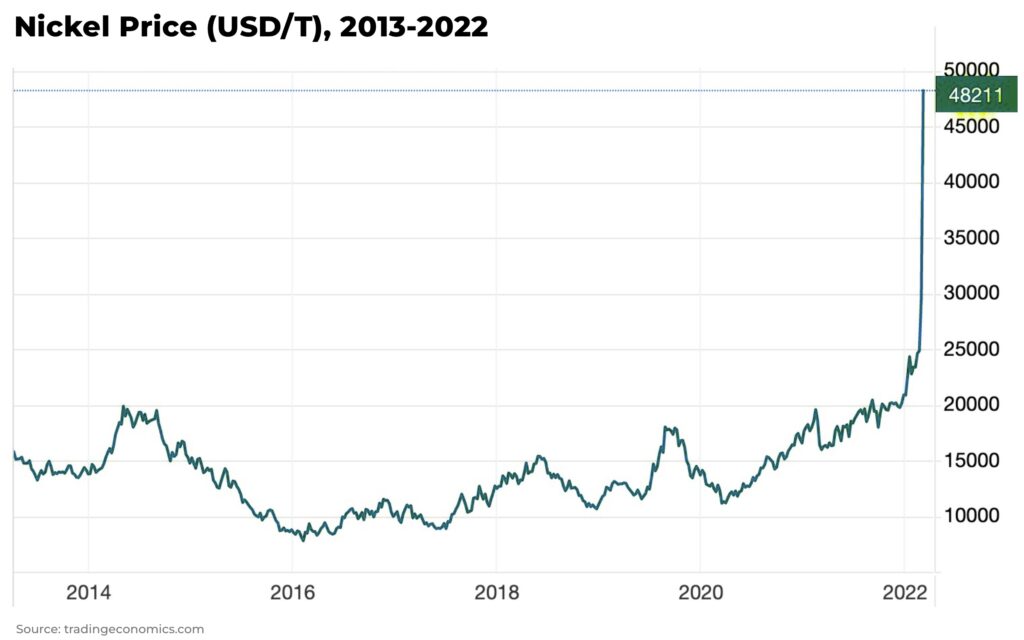

Low liquid instruments

Instruments with small liquidity are another threat for Brokers using only B-Book. Usually, they are rarely traded by a broker’s clients, but their low liquidity in extreme situations can cause massive volatility. Example: Nickel on 8th March 2022.

Solution: Always hedge all the exotic symbols traded by the Broker’s clients. Liquidity and volatility affect each other, with reduced liquidity usually leading to a more volatile market with large price swings. The price can move in a narrow price range for a long time Before a sudden move, so relying on quote history can be very deceptive.

White whales

In sales terms, a whale is a lead that has the potential to bring enormous sales revenue to a company, a trader who bets extraordinarily large amounts of money. However, with a high potential also comes increased risk.

When a broker has a large number of clients with relatively similar deposits, the volume of trades, on average, tends to be balanced. However, when one client has deposited significant amounts of money (at least 25% of all aggregated deposits), it can easily disturb the exposure and put a broker at high risk. (Significant amounts vary between Brokers).

Concentrated flow

If all the clients are trading in the same direction (for example, they follow an influencer etc.), it poses a risk similar to big trades of a “whale”.

Solution: A broker should monitor his risk on a daily basis (if he is not fully A-Book). When his exposure is not balanced, he should hedge it all or part to decrease his risk of potential losses.

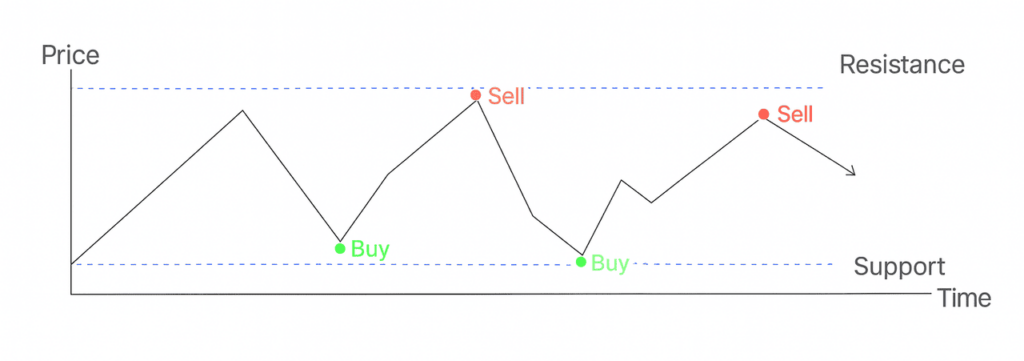

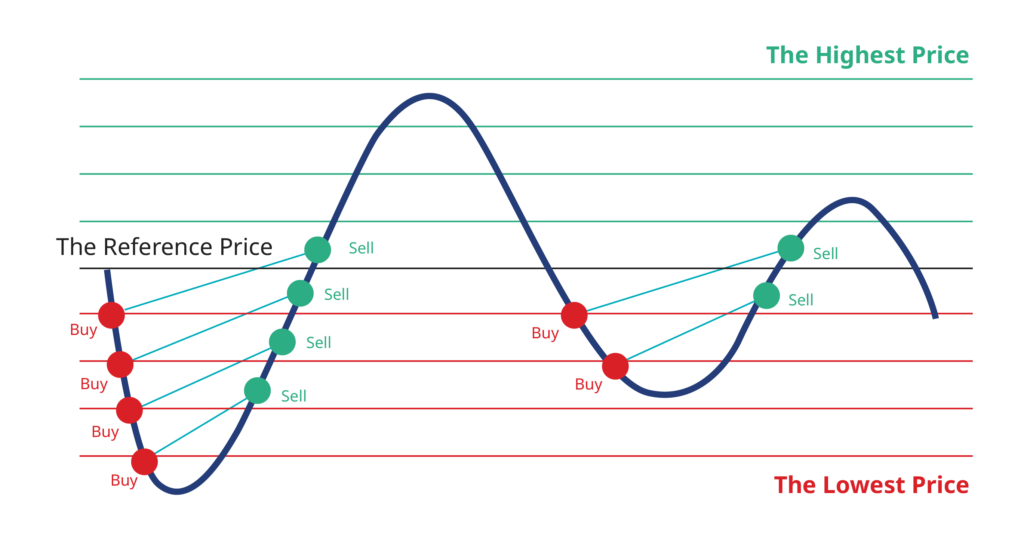

Range Market and Grid Strategies (dangerous mix)

When the market moves in a limited range, it is a very dangerous situation for B-Book brokers because clients have a much bigger probability that their trades will be profitable. Clients can use local heights and lows to enter positions, and they can wait until the price reaches the opposite side of the corridor. If such a situation on the market occurs it is worth considering to hedge such instruments. Profitability on B-Book during such low volatility periods can be significantly lower than on A-Book.

Additionally, if your clients use so-called “grid strategies”, which are intended to make most of the profits during the range markets, then B-Book profitability can be put on even higher risk. It is always wise to monitor your clients’ behaviours and check what strategies they use and if they use some additional trading tools, such as robots, EAs, to enter positions.

Below you can see what such a grid strategy looks like.

Control of Broker’s Market Exposure

To control exposure related to market risk, particularly regarding specific instruments, an FX broker can take the following measures:

1) Set exposure limits: Establish and enforce exposure limits for each instrument and currency pair, taking into account the Broker’s risk appetite, market conditions, and regulatory requirements.

2) Diversify offerings: Offer a variety of instruments and currency pairs to encourage clients to diversify their portfolios, which can help reduce the overall exposure to any single instrument or currency pair.

3) Monitor positions in real-time: Implement a robust monitoring system to track positions and exposure to specific instruments and currency pairs in real-time. This allows the Broker to take prompt actions in case any exposure limits are breached.

4) Implement hedging strategies: Use internal and external hedging techniques to manage the Broker’s exposure to specific instruments or currency pairs. Internal hedging can involve matching client orders to offset risk, while external hedging may require entering into contracts with liquidity providers or other counterparties.

5) Conduct regular portfolio analysis: Regularly analyse the Broker’s overall portfolio to identify concentrations in specific clients or instruments. This analysis can help the Broker to take appropriate actions to rebalance the portfolio and maintain the desired level of exposure.

6) Utilise risk management tools: Employ risk management tools, such as options, swaps, and futures contracts, to hedge the Broker’s exposure to specific instruments and currency pairs.

7) Monitor market conditions: Keep a close eye on market developments, economic indicators, and geopolitical events that may impact the value of specific instruments or currency pairs. This information can help the Broker to anticipate potential changes in exposure and take appropriate actions.

8) Set margin requirements: Establish and enforce margin requirements for each instrument and currency pair to ensure that clients have sufficient funds in their accounts to cover potential losses. This can help limit the Broker’s exposure in case of adverse market movements.

9) Establish stop-loss limits: Encourage clients to use stop-loss orders for their trades, which can help limit potential losses and the Broker’s exposure to specific instruments or currency pairs.

In Match-Trader, there is an exposure tab which can help you to monitor the exposure of your brokerage.